The theoretical framework of this research posits that financial time-series exhibiting significant autoregressive affinity—particularly those characterized by endogenous dynamics—can be decomposed into discrete, equal-length subsequences. Following the literature on Time Series Motifs (Keogh et al., 2003) and Regime-Switching Models (Hamilton, 1989), it is hypothesized that these subsequences gravitate toward latent "families" or centroids within a high-dimensional feature space.

Assets such as Cryptocurrencies and Commodity ETFs serve as primary candidates for this methodology. Unlike traditional equities, which are subject to exogenous shocks from corporate governance and quarterly earnings reports, these assets are predominantly driven by the reflexive supply-and-demand dynamics of market participants. In short temporal windows, these dynamics often manifest as recurring structural patterns, or "micro-regimes" (Lillo et al., 2015).

Methodologically, the partitioned segments are mapped as vectors \( \mathbf{v} \in \mathbb{R}^n \). Through unsupervised learning (e.g., K-Means clustering), these vectors are assigned to a cluster index \( C_k \in \{1, \dots, K\} \). The predictive component utilizes a first-order Markovian approach to estimate the transition probability matrix: \[ P(C_{t+1} = j \mid C_t = i) \] This "Cluster-then-Predict" workflow (Niu et al., 2020) enables the estimation of future return distributions based on the current observed state. In an operational context, a long position is initiated when the conditional expectation of the subsequent cluster implies a positive return, \( \mathbb{E}[R_{t+1} \mid C_t] > 0 \), while a short position is considered otherwise.

Paper PDF

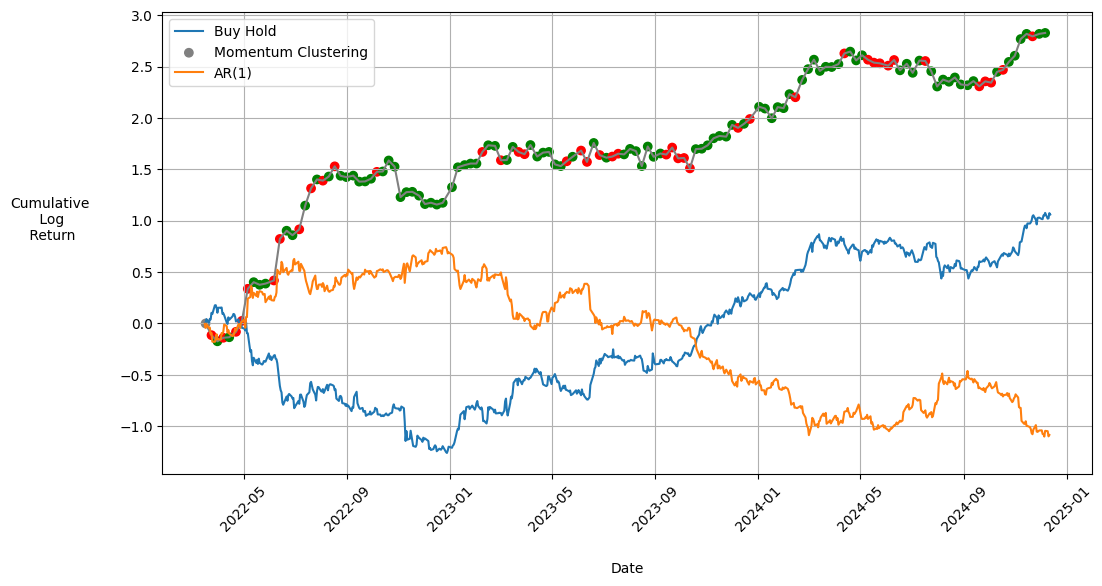

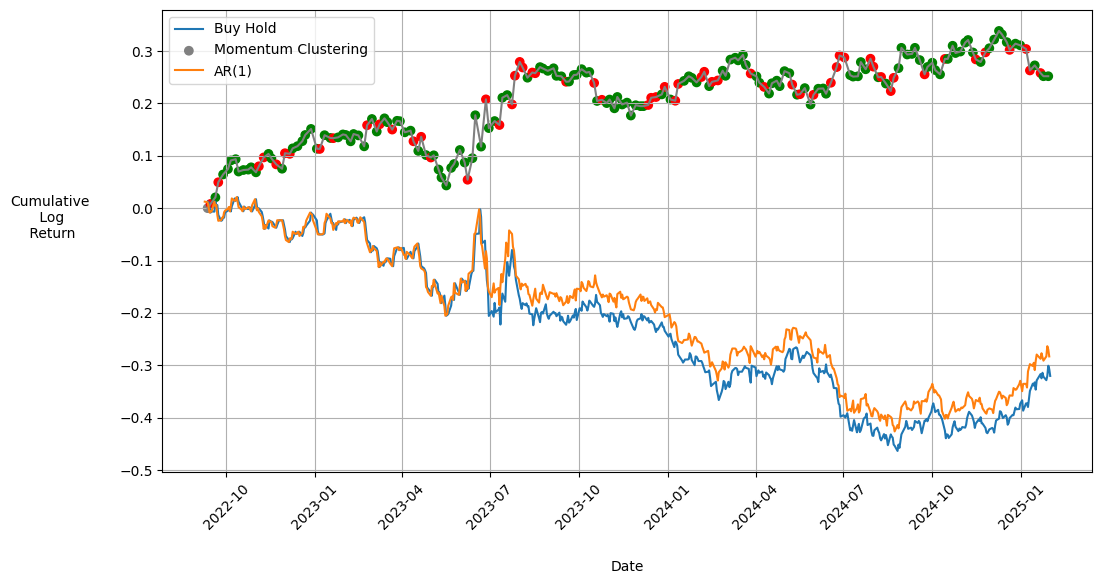

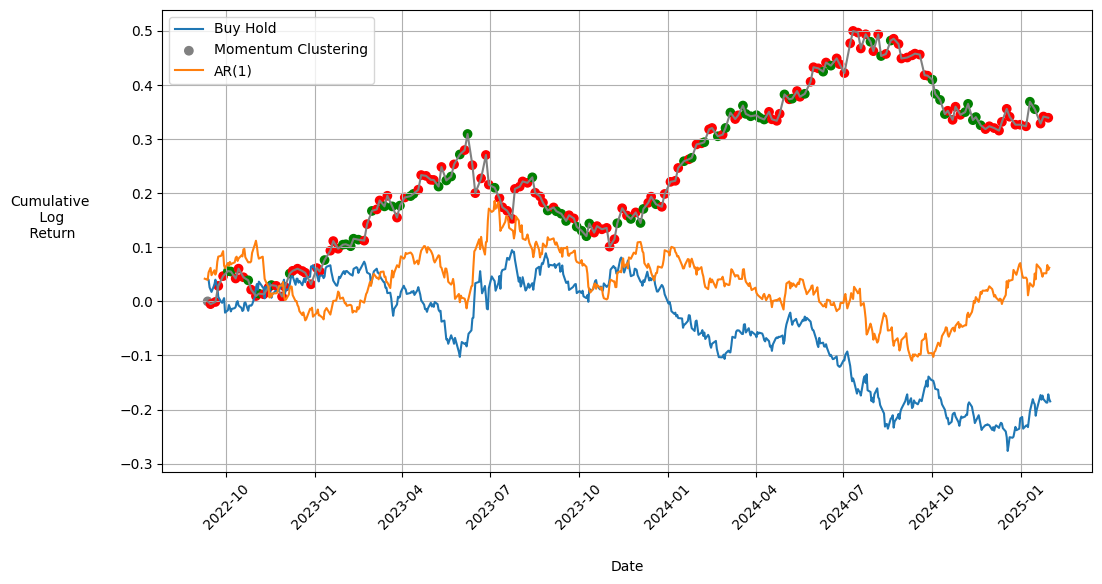

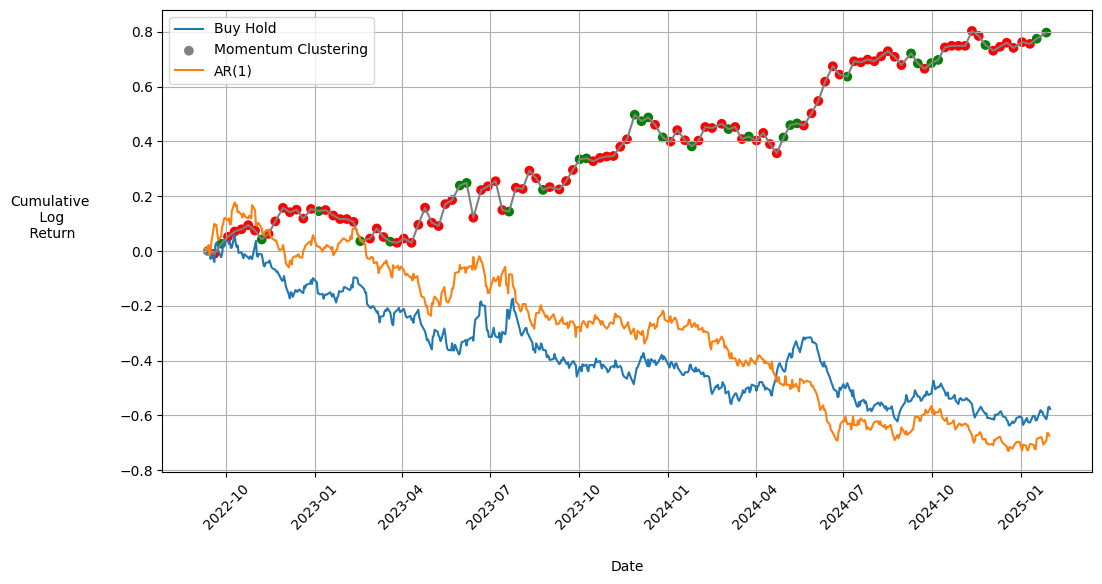

Results

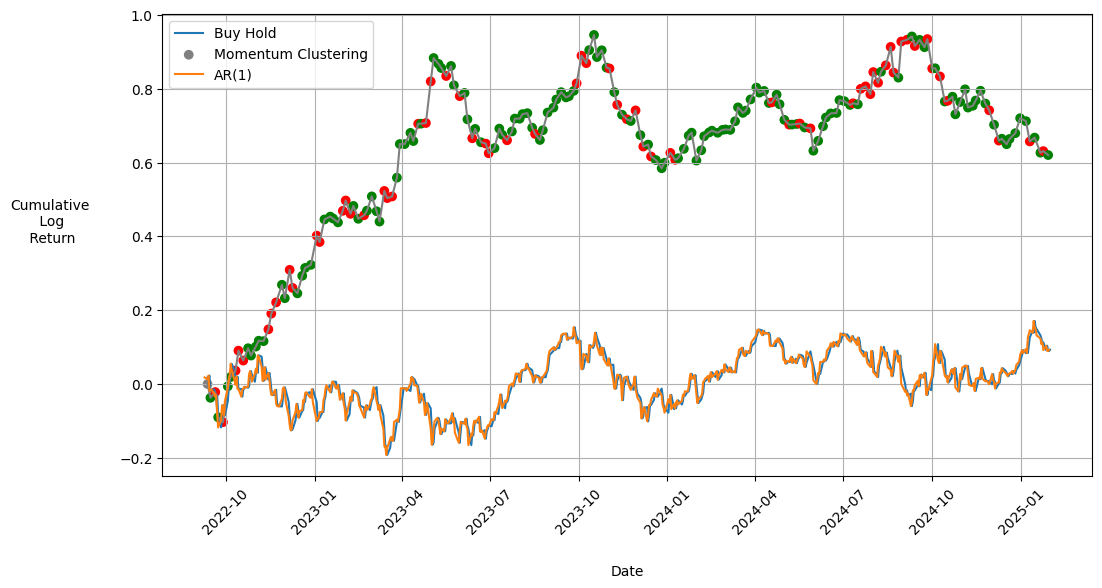

Green - Long Position Taken

Red - Short Position Taken

Y-Axis - Cumulative Log Return

References

- Hamilton, J. D. (1989). A New Approach to the Economic Analysis of Nonstationary Time Series and the Business Cycle. Econometrica, 57(2), 357–384.

- Keogh, E., et al. (2003). Segmenting Time Series: A Survey and Novel Approach. Data Mining in Time Series Databases, 1–22.

- Lillo, F., et al. (2015). Market Microstructure and Regimes in Financial Time Series. Journal of Statistical Mechanics: Theory and Experiment.

- Niu, H., et al. (2020). A Cluster-then-Predict Framework for Financial Time Series Forecasting. IEEE Access.