Presentation @ QF & Statistics PhD Webinar

I presented work from TIPS ETF whitepaper at SBU QF & Statistics PhD Webinar, featuring guests from Goldman Sachs and Renaissance Technologies

Data Scientist with 5 years of experience leveraging machine learning, analytics, and engineering to provide intelligent insight. Interested in the fields of causal inference, Monte Carlo, optimization, statistics, time-series analysis, computational mathematics, and simulation.

I presented work from TIPS ETF whitepaper at SBU QF & Statistics PhD Webinar, featuring guests from Goldman Sachs and Renaissance Technologies

My paper explores new way to classify momentum and micro-regimes in time-series, using clustering as an alternative to autoregressive methods. (IN PROGRESS)

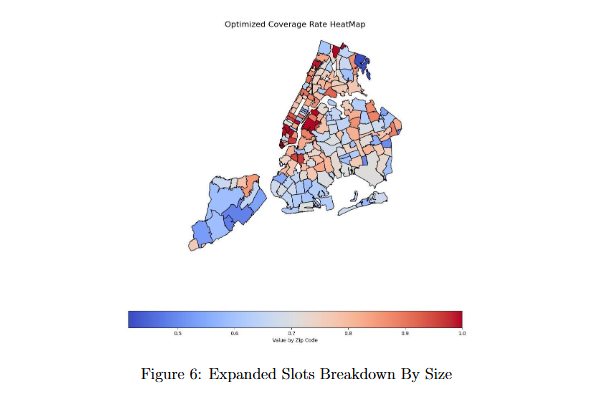

I co-authored a paper that optimally assigns childcare facilities to maximize facility access in NY counties with minimal cost (IEOR 4004)

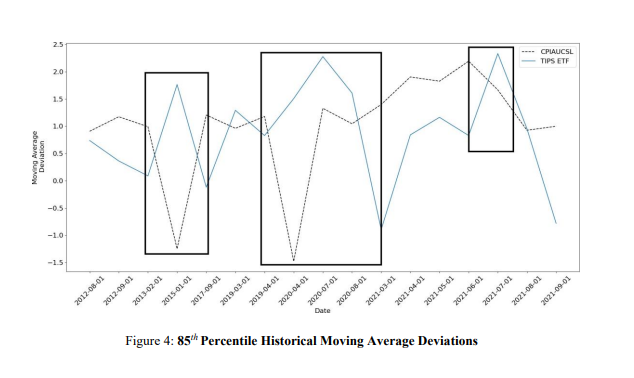

I co-authored a whitepaper with Dr. James Glimm that conducts extreme value analysis of iShares TIPS ETF & CPI to find signals for ETF share price and improve autoregressive models

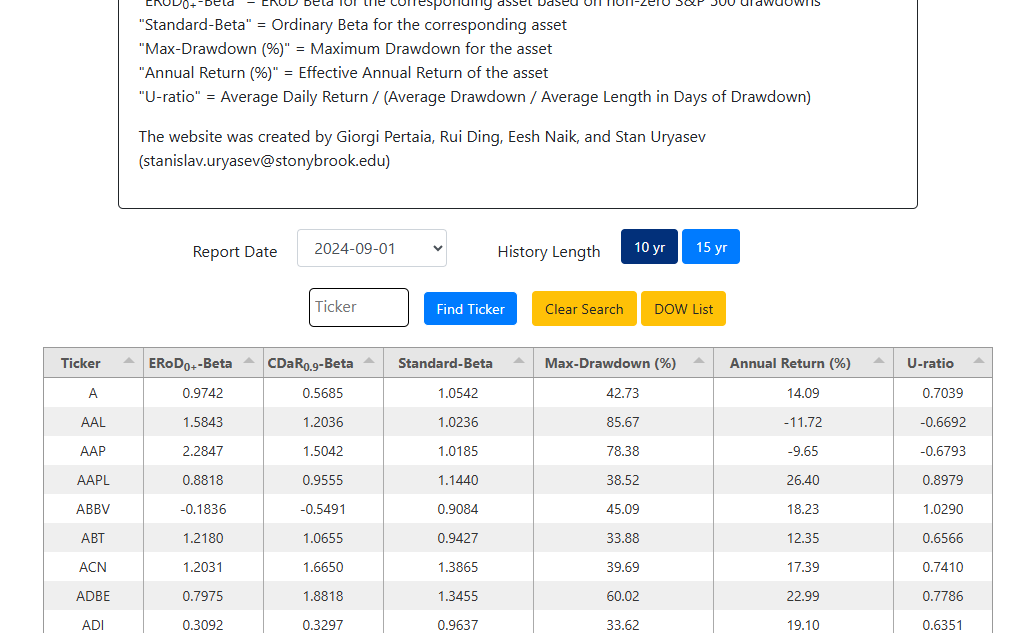

I co-developed website that features Conditional Drawdown At-Risk Beta, Expected Regret Drawdown Beta & more for all S&P 500 tickers